Introduction: Equity Financing

Equity financing occurs when ownership stakes in a particular firm are exchanged for financial capital from investors. These investors may be all types of people, from friends and family of the business, to wealthy, "angel" investors, to venture capitalists. The main advantage of equity financing is that the business is not obligated to repay anything, since the individual investors are assuming a certain amount of risk in return for the possibility of making money in the future. However, because equity financing involves trading funds for ownership in the company, these new investors do gain some decision-making power in the company, and the managers lose some autonomy.

Common Stock and Preferred Stock

Typically, firms obtain their long-term sources of equity financing by issuing common and preferred stock. Holders of common stock (also be known as a "voting share" or an "ordinary share") often have voting rights on corporate policy and have a say in electing the firm's Board of Directors. They also receive dividend payments if the firm offers them. That being said, in the event of liquidation, preferred stock is considered more senior than common stock, in terms of rights awarded to particular investors. If one investor has preferred stock, while another holds common stock, that first individual has more rights to their share of assets, in the event of a liquidation. After bondholders, creditors (including employees), and preferred stock holders are paid their full share, common stock investors receive any funds that still remain. Thus, it is clear that common stock investors have the riskiest investment, often receiving nothing in the event of a bankruptcy.

Preferred stock is considered to be a form of equity security. It has properties of both an equity and a debt instrument, making it a "hybrid instrument". Preferred stock generally has preference in receiving dividend payments and always has preference in asset claims during liquidation. That being said, holders of this type of stock usually do not have voting rights, while common stock holders do. Almost all preferred shares have a negotiated, fixed-dividend amount. The dividend is usually specified as a percentage of the par value, or as a fixed amount (for example, Pacific Gas & Electric 6% Series A Preferred). Sometimes, dividends on preferred shares may be negotiated as floating. This means that they may change according to a benchmark interest-rate index (such as LIBOR).

Types of Preferred Stock

In general, there are four different types of preferred stock: cumulative preferred stock, non-cumulative preferred stock, participating preferred stock, and convertible preferred stock. With cumulative preferred stock, If the dividend is not paid, it will accumulate for future payment. With non-cumulative preferred stock, dividends will not accumulate if they are unpaid. In other words, holders of this type of stock cannot make claims to forgone, past dividends. Convertible preferred stock are preferred issues which holders can exchange for a predetermined number of the company's common-stock shares. This exchange may occur at any time the investor chooses, regardless of the market price of the common stock. It is a one-way deal, and an individual cannot convert the common stock back to preferred stock, if they have already exchanged their preferred stock with the company. The final type, participating preferred stock, are preferred issues that offer holders a set, specified dividend. These also offer investors the the opportunity to receive extra dividends if the company achieves predetermined financial goals. In the event of liquidation, holders of this last type of preferred stock are entitled to receive back the total amount they invested in the company, as well as the accumulated unpaid dividends, before any common stock holders are paid.

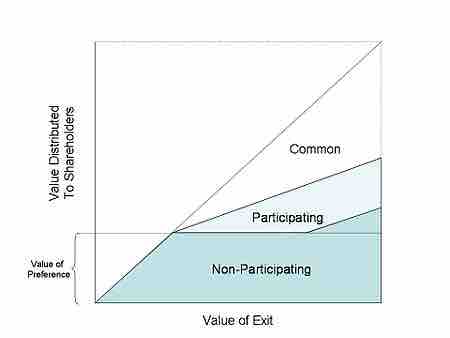

Participating Preferred vs. Non-Participating Preferred

This graph shows an example of a liquidation event, illustrating how assets will be divided up between common, participating preferred, and non-participating preferred stock holders. All preferred stockholders are paid first, before common stock holders. Participating preferred stockholders can "double dip", and are entitled to both their money back, as well as the leftovers for common stock, proportionate to the amount of common stock for which their preferred stock can be converted into.

There are capital costs associated with equity financing, including accounting and legal costs, as well as underwriting and filing fees. For new issues of stocks, there are flotation costs that must be taken into consideration before choosing equity as a method of long-term financing. These can be established with the following formulas. Cost of preferred stock = Next dividend to be paid/[Current market value(1-flotation costs)]Cost of newly issued common stock = Next dividend to be paid/Current market value(1-flotation cost) + projected growth rate.