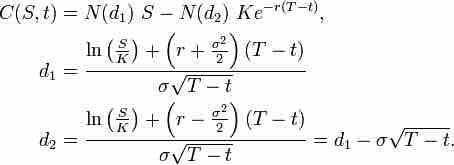

Valuation of a Call Option

Where: N is the cumulative distribution function of the standard normal distribution; T - t is the time to maturity; S is the spot price of the underlying asset; K is the strike price; r is the risk free rate; and omega is the volatility of returns of the underlying asset.

Source

Boundless vets and curates high-quality, openly licensed content from around the Internet. This particular resource used the following sources: