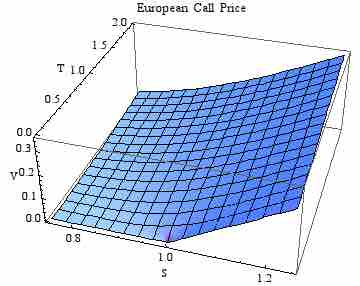

European Call Surface

A European call valued using the Black-Scholes pricing equation for varying asset price S and time-to-expiry T. In this particular example, the strike price is set to unity, the risk-free rate is 0.04 and the volatility is 0.2.

Source

Boundless vets and curates high-quality, openly licensed content from around the Internet. This particular resource used the following sources:

"European Call Surface."

http://en.wikipedia.org/wiki/File:European_Call_Surface.png

Wikipedia

GNU FDL.

{kind=link}