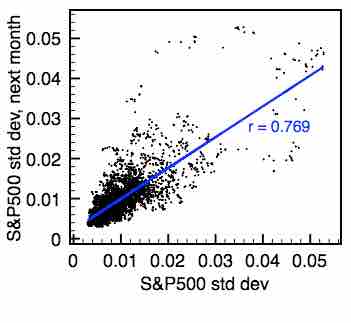

Volatility begets volatility

Data shown is from the period of Jan. 1990-Sep. 2009. Volatility is measured as the standard deviation of S&P 500 one-day returns over a month's period.

Source

Boundless vets and curates high-quality, openly licensed content from around the Internet. This particular resource used the following sources: