An empirical example relating diversification to risk reduction

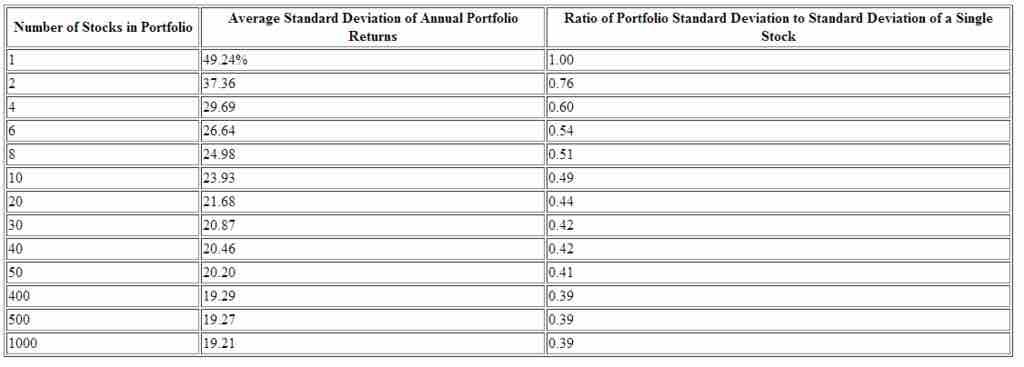

In 1977 Elton and Gruber worked out an empirical example of the gains from diversification. Their approach was to consider a population of 3,290 securities available for possible inclusion in a portfolio, and to consider the average risk over all possible randomly chosen n-asset portfolios with equal amounts held in each included asset, for various values of n. Their results are summarized in the following table. It can be seen that most of the gains from diversification come for n≤30.

Source

Boundless vets and curates high-quality, openly licensed content from around the Internet. This particular resource used the following sources:

"Diversification (finance)."

http://en.wikipedia.org/wiki/Diversification_(finance)

Wikipedia

GNU FDL.